Original article available here: https://www.yolegroup.com/strategy-insights/cmos-image-sensor-snapshot-not-all-doom-and-gloom-good-news-is-also-stacking-up/

CMOS Image Sensor snapshot: not all doom and gloom, good news is also stacking up

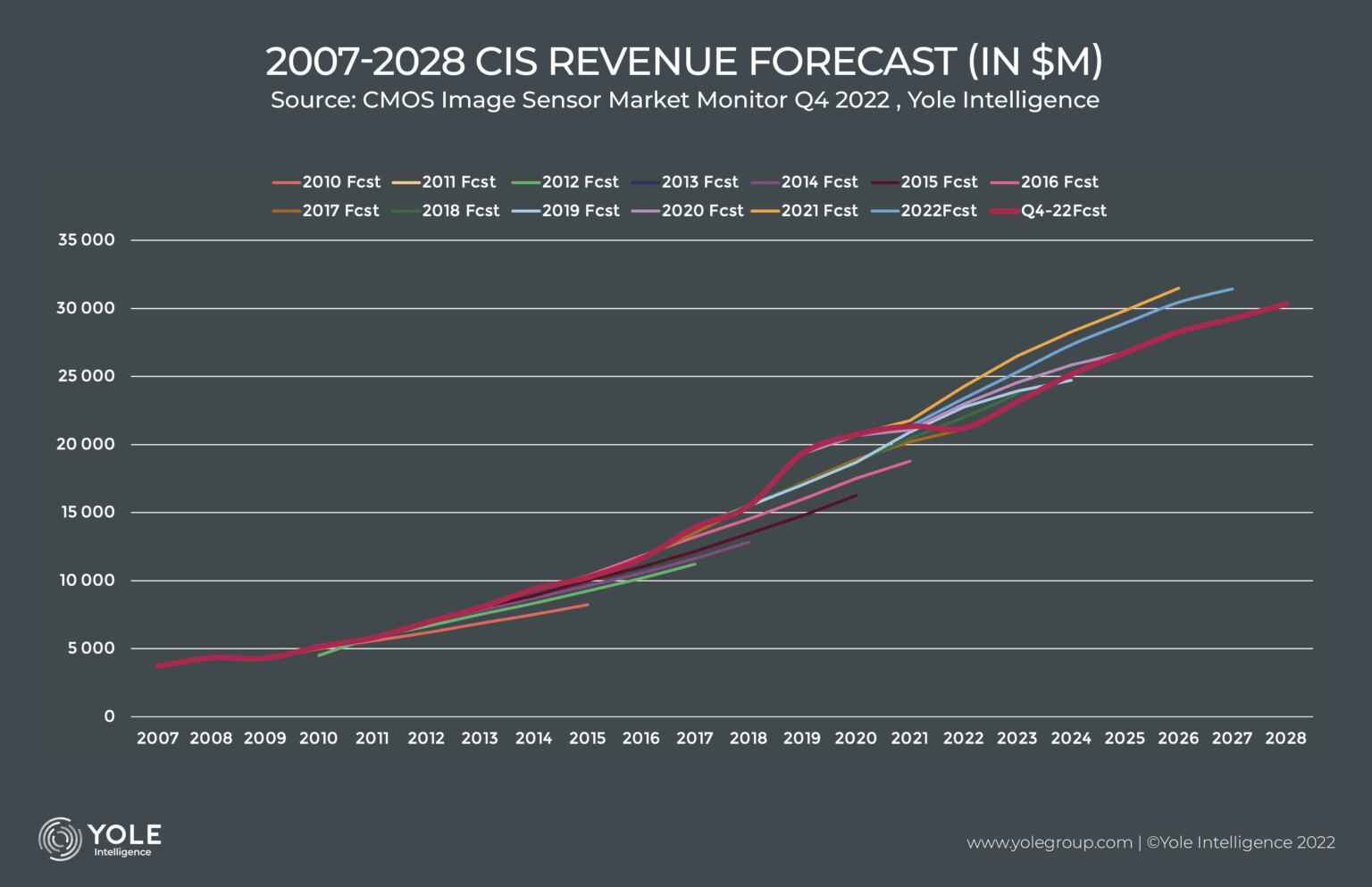

In the CMOS Image Sensor Monitor Q4 2022, Yole Intelligence, part of Yole Group, announces it expects the CMOS Image Sensors (CIS) industry to show a slight revenue decrease of -0.7% YoY in 2022, with a market value of $21.2B. This estimate takes into account the many events in 2022’s first 3 quarters; the downward revision of smartphone sales, the ongoing inventory reduction from most players in the electronics supply chains, and the continued Covid-19-related disruptions in China.

2021 was a year of growth for CIS, reaching an all-time high of $21.3B in revenue with a relatively small annual growth of 2.8%. The key driver was the rebound in sales of smartphones, computer laptops, and tablets during the year amid the reopening of western economies after severe Covid-19-related lockdowns. Our hope for 2022 was a continuation of this improving trend. We knew the Huawei ban contributed to some inventory build-up in 2020, which had to be cleared in 2021 and maybe 2022. Our expectation for the smartphone market in 2022 was, unfortunately, too high, which translated directly into lost revenue for CIS.

In the past, the increase in the number of cameras per phone would more than compensate for smartphone volume sales declines, but not in 2022. Huawei was the actor adding the greatest number of cameras per phone, and losing such a player in the geopolitical battle has flattened the growth statistic of cameras per phone. Does it mean consumers have lost interest in high-quality phone cameras? Not at all!

Video creation using smartphones is at an all-time high due to the short-video craze. The emergence of TikTok, the favored social media of the younger generation, has been quickly copied by large incumbents, resulting in YouTube shorts and Facebook reels. This demand for high-quality video hardware was temporarily over-met during the out-of-Covid-19-lockdowns of 2021, and, therefore, the first 3 quarters of 2022 saw slightly less demand. We have seen even more dramatic but similar patterns with computer laptops and tablets in which cameras played a central role during remote work/school teleconferencing.

Another market that has explosive growth right now is Automotive CIS. The Covid-19 era signaled a turning point in consumer behavior, with demand switching to Connected Autonomous Shared and Electric (CASE) vehicles loaded with semiconductor-based features. Overall, the appetite for cameras remains high, but the dominance of the weakened smartphone market translates into the deceptive -0.7% CIS growth expected for 2022.

The smartphone market is down -10% but the sales of CIS have proven relatively resilient, while other semiconductor products, such as memory, are down -12%. The main reason is technical since we are currently experiencing a limited supply of 90nm to 40nm node wafers, the main nodes for CIS, and supporting logic wafers. The prices of these legacy nodes have increased significantly, and we observed, therefore, a continuation of high average selling prices (ASP) for CIS.

At the same time, we noted a product mix shift toward more resolution and larger optical formats; this means more silicon per die and higher ASPs. In this respect, the large smartphone OEMs have different approaches; Apple and Xiaomi favor 12Mp to 48Mp resolution with large pixels, which seems to be the ultra-premium favored approach, while Samsung, Oppo, and Vivo are increasing the resolution to 64Mp and even 108Mp with smaller pixels, which appears as the mid-end favored approach. The market is, therefore, relatively well educated and understands what a good picture means, as described in our publication with DXOMARK, “Ultra-Premium Flagship Smartphones Image Performance: End-User Perspective 2021”.

This year, both Sony and OmniVision have presented products with three-layer stacks. There are two technical reasons for this. First, the “in-pixel connection” allows removing some transistors from the upper wafer layer and moving these to the second wafer layer. This improves the volume of sensing silicon in each pixel. This technology is helpful in optimizing the signal-to-noise ratio (SNR), a critical factor in improving image quality. The second reason is that the triple stack enables high-performance sensing. New uses, such as tiny AR/VR cameras, must go beyond the current rolling-shutter (RS) approach and use either global-shutter (GS), time-of-flight (ToF), or even event-based (EB) cameras. All these require more transistors per pixel than RS approaches, so a second CIS layer is more than welcome in the drive to super compact sensing cameras. The market share of these triple-stack image sensors will grow, which will add again to the increasing silicon content per camera. This trend opens a path for sustained improvement and market growth for CIS.

The 8 leading CIS players – Sony, Samsung, OmniVision, STMicroelectronics, onsemi, SK Hynix, GalaxyCore, and SmartSens – that we have been monitoring every quarter have very different business models. Sony is a hybrid IDM, manufacturing its own 12’’ CIS wafers but outsourcing logic wafers to TSMC, UMC, and possibly also Global Foundry (unconfirmed as yet). Samsung, STMicroelectronics, and SK Hynix are IDMs with some open foundry activity. OmniVision, onsemi, GalaxyCore, and SmartSens, are fabless with varying degrees of desire for internalization; onsemi now having ownership of the East Fishkill, New York fab, and GalaxyCore investing the proceeds of its IPO into a brand new 12’’ foundry. All these players have felt pain from their supply chain structure in 2021 and 2022, either from their dependencies on others or their own limited or vulnerable capabilities. The drought and fires that happened in Samsung’s Austin, Texas, fab last year and the similar events that occurred in Taiwan’s TSMC fabs are clear reminders that no one is immune to supply-side issues in the context of climate change and geopolitical uncertainties.

The next few years will be a race to add new industrial capacities, combined with renewed technological capabilities and a high level of consumer demand. Predictions are very difficult, especially if it’s about the future! With our CIS monitor quarterly publication, we make sure to stick to reality and include some accountability in our forecast. In our view, the future is bright for CIS, but large vulnerabilities exist from the economic and geopolitical context. Let us all make this a well-informed journey with the CIS Monitor publications.

No comments:

Post a Comment

All comments are moderated to avoid spam and personal attacks.